.avif)

.png)

.png)

.avif)

Employer employee insurance in India usually refers to the bundle of group policies an organisation buys for its workforce—most commonly group health insurance, group term life, and group personal accident. In some contexts, the term also points to the “employer–employee” life-insurance arrangement (distinct from keyman policies) that lets a company purchase life cover on employees under a single master policy. Either way, this isn’t a feel-good extra; it’s a structured way to protect people, stabilise productivity, and signal that the organisation thinks long-term.

What “employer employee insurance” actually means

In day-to-day Indian usage, the term spans two related ideas. First, there’s the group benefits stack: a health policy (often with cashless hospital networks), a group term life policy that pays a lump sum to a nominee, and a personal accident policy that adds disability and accidental-death cover. Second, there’s the employer–employee life-insurance arrangement administered by insurers under a single master contract, not to be confused with keyman cover where the company is the beneficiary. Life insurers describe the employer–employee arrangement as a way to insure many employees under one policy, with benefits flowing to employees or their nominees rather than to the company (unlike keyman).

Why Employer-Employee Insurance is Essential

{{group-insurance-quote="/web-library/components"}}

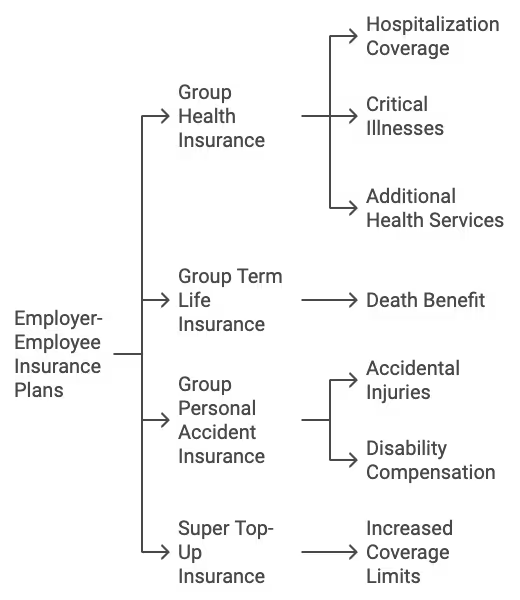

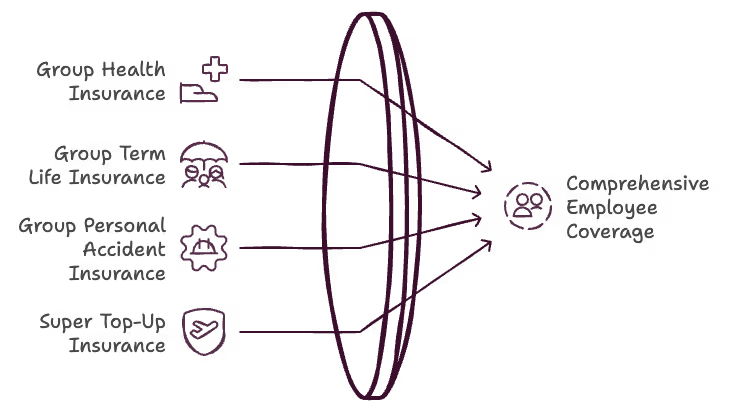

Types of Employer-Employee Insurance Plans

Employer-Employee insurance plans cover a range of protections designed to address different aspects of employee well-being. Here are some core types:

Detailed Plan Comparisons

To help businesses understand how each insurance type works, here’s a breakdown of the core types of employer-employee insurance plans, highlighting their benefits, limitations, cost considerations, and ideal use cases:

{{group-insurance-quote="/web-library/components"}}

In-Depth Coverage Descriptions

To give a clearer idea of each type’s practical application, here’s how each coverage type can help employees in real situations:

Common Pain Points and Solutions for Employers and Employees

Both employers and employees can face challenges when implementing or accessing employer-sponsored insurance.

Addressing these challenges can improve uptake, reduce confusion, and optimise the benefits for everyone involved.

- Challenges in Implementation for Employers

Budget Constraints: Many small to medium businesses struggle to balance cost with comprehensive coverage.

Solution: Consider phased insurance schemes or selective coverage options, focusing on core needs first. Negotiating bulk deals or using a platform that offers customised plans can also help manage costs effectively.

Employee Onboarding and Awareness: Employees may not fully understand or utilise insurance benefits, limiting the plan’s effectiveness.

Solution: Organise brief, interactive sessions explaining the benefits and usage of the insurance, supported by user-friendly digital resources (videos, FAQs, apps).

Managing Claims: Administrative tasks involved in processing claims can be time-consuming and costly.

Solution: Use an insurance partner that offers automated claims processing, simplifying the claim journey for employees while reducing HR’s workload.

- Challenges for Employees in Accessing Benefits

Lack of Information: Employees are sometimes unclear about policy specifics, leading to underutilisation.

Solution: Provide access to a self-service portal where employees can review their coverage, claim processes, and FAQs at their convenience.

Complex Claim Processes: Some employees may avoid claiming benefits if the process is overly complex or time-consuming.

Solution: Look for insurance providers that offer a streamlined, digital claims process with simple, clear instructions and minimal paperwork.

Coverage Gaps in Group Policies: While group plans cover a lot, they may lack certain specific benefits (e.g., outpatient care or high critical illness coverage)

Solution: Offer employees the option to add coverage layers or supplementary plans, like super top-up insurance, to enhance their protection if needed.

{{group-insurance-quote="/web-library/components"}}

Legal and Regulatory Framework in Greater Depth

Understanding the legal landscape around Employer-Employee insurance in India is essential for both compliance and effective benefits management.

This section explores the core legal requirements and recent policy changes that impact employers and employees.

By keeping up with these legal requirements and staying informed about regulatory changes, companies can create a compliant and comprehensive insurance structure that boosts employee trust and loyalty.

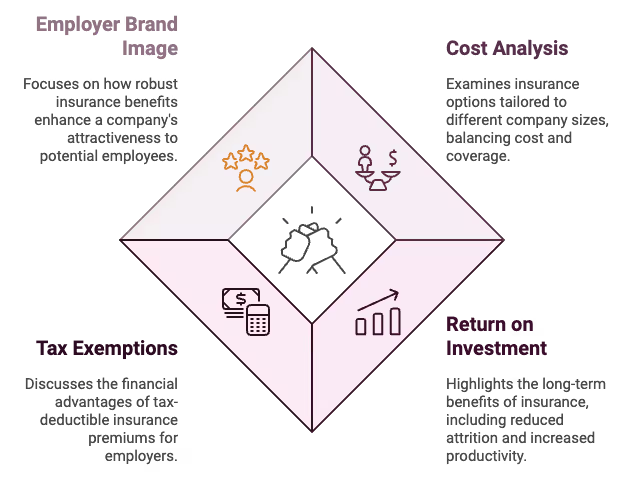

Cost-Benefit Analysis for Employers

Employer-Employee insurance can be a significant investment, especially for smaller businesses.

However, a detailed cost-benefit analysis reveals that the long-term advantages often outweigh the initial expenses, enhancing both employee satisfaction and company growth.

In summary, Employer-Employee insurance is not only a tax-efficient benefit but also a powerful tool to drive business growth by ensuring a healthy, loyal, and productive workforce.

Employee Perspective: Maximising Benefits

While employer-sponsored insurance provides significant benefits, many employees may not fully understand how to make the most of these policies.

Here are practical tips for employees to access maximum value from their Employer-Employee insurance plans:

By proactively engaging with their employer-sponsored insurance and understanding its full potential, employees can secure health and financial stability for themselves and their families.

{{group-insurance-quote="/web-library/components"}}

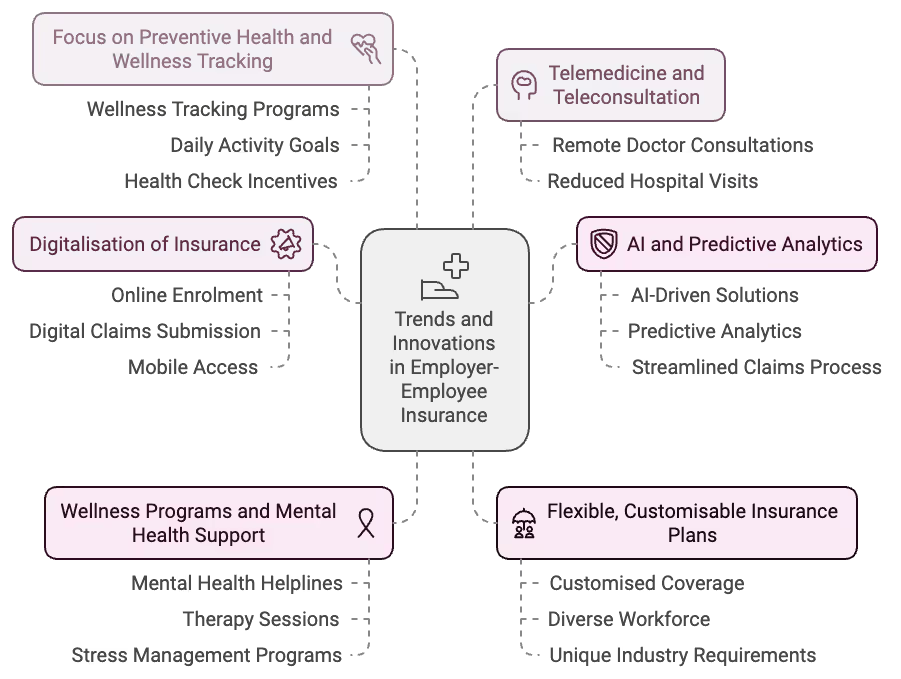

Trends and Innovations in Employer-Employee Insurance

The employer-employee insurance sector in India is evolving rapidly, thanks to technology and shifting workplace expectations.

Here are some of the latest trends and innovations making group insurance more accessible and personalised:

By embracing these innovations, employers can offer a modern, user-friendly insurance experience that promotes employee health, satisfaction, and loyalty.

Guide to Employee Insurance in Startups and SMEs

For startups and small to medium-sized enterprises (SMEs), offering employee insurance can be a game-changer.

Despite smaller budgets, these businesses can still provide meaningful insurance benefits with careful planning and provider selection.

Here’s a guide on how startups and SMEs can get the most from their insurance investments:

By investing in employee insurance early, startups and SMEs can build a supportive, health-focused work environment that attracts motivated employees and reduces turnover.

{{group-insurance-quote="/web-library/components"}}

Frequently Overlooked Details and Hidden Costs in Group Insurance

While group insurance offers substantial benefits, it’s essential for both employers and employees to understand the finer details.

Certain hidden costs and policy conditions can impact the true value of coverage if not accounted for upfront.

Here are some commonly overlooked factors:

Being aware of these hidden details helps employers optimise their insurance investment, creating a transparent, reliable benefits package for employees.

FAQs on Claim Processes and Claim Settlements

Navigating the claims process can sometimes be complex for employees.

Here are answers to common questions that help clarify claim filing, settlement, and dispute resolution under employer-sponsored insurance:

Q. How do companies determine the coverage amount for each employee?

A. Coverage amounts are typically based on factors like the employee’s role, salary, and importance to business operations. Higher coverage might be assigned to senior positions or roles with greater responsibilities.

Q. Can employees customise their coverage under the Employer-Employee Insurance plan?

A. Usually, the employer decides the core coverage terms based on the group policy. However, some companies allow employees to opt for additional voluntary coverage, which can provide flexibility for those seeking enhanced protection.

Q. What is the difference between cashless claims and reimbursement claims?

A. Cashless Claims: These allow employees to receive treatment at network hospitals without upfront payment, as the insurer directly settles the bill with the hospital.

Reimbursement Claims: If an employee visits a non-network hospital, they need to pay upfront and then submit bills and documentation for reimbursement.

Q. How can employees speed up the claim settlement process?

A. To expedite claim settlement, employees should ensure all required documentation is complete and accurate. Using digital platforms or insurance apps provided by the insurer can also streamline claim submission and tracking.

Q. What should an employee do if a claim is disputed?

A. In case of disputes, employees should first approach the insurance provider’s support team, ideally through the employer’s HR department. If necessary, the employee can file a complaint with the Insurance Ombudsman for impartial resolution.

Q. What happens to the insurance coverage if an employee leaves the company?

A. Coverage usually ends once employment is terminated. However, some group policies may offer a conversion option, allowing employees to continue coverage by paying the premiums themselves. This option depends on the policy terms and should be confirmed with HR or the insurer.

{{group-insurance-quote="/web-library/components"}}

Conclusion

Employer-Employee insurance offers significant advantages to both organisations and employees, from tax benefits and increased employee loyalty to comprehensive health coverage and financial security for families.

By providing meaningful protection, companies can foster a healthier, more engaged, and committed workforce.

If you’re looking to offer robust insurance benefits at affordable rates, consider exploring comprehensive plans tailored to your organisation’s unique needs.

Start by comparing quotes, assessing plan options, and consulting with experts to ensure a well-rounded, competitive insurance package for your team.